Both plans offer enhanced support for severe disabilities in addition to the existing government schemes, so you can have better assurance for you and your loved ones.

National long-term care insurance schemes that provide basic financial support for severe disability

Payout when unable to perform three or more ADLs

Supplement plan for better disability support

Payout when unable to perform at least 2 ADLs

Supplement plan for better disability support

Payout when unable to perform at least 1 ADLs

Singlife CareShield Standard or Singlife CareShield Plus offer benefits 1 to ensure you receive the care you need during unexpected events in life.

S$200 to S$5,000 more on top of basic severe disability payouts from the government, for as long as you’re severely disabled.

You are unable to perform at least two (for Singlife CareShield Plus) or three (for Singlife CareShield Standard) of the six Activities of Daily Living (ADLs).

Receive additional monthly payout of up to 12 months with the Add-on Benefit 2 if you are unable to perform any Activities of Daily Living (ADLs).

The ADLs are washing, toileting, feeding, dressing, transferring around and walking or moving around.

Stop paying your premiums but remain covered when you have a mild disability.

You are unable to perform at least one Activity of Daily Living (ADL).

The ADLs are washing, toileting, feeding, dressing, transferring and walking or moving around.

Pick fixed or increasing payouts, and your preferred premium payment period up to the policy anniversary after you turn 98, or for a limited time 3 .

Payouts that grow by 2% or 3% annually to help you manage inflation.

Pay your premiums with your MediSave 4 , and you’ll spend little or no cash from your pocket.

Get a lump-sum benefit that's 3x your monthly benefit 5 , when you're severely disabled - this can help with one-time costs, such as in the purchase of a wheelchair.

You are unable to perform at least two (for Singlife CareShield Plus) or three (for Singlife CareShield Standard) of the six Activities of Daily Living (ADLs).

If you're severely disabled, get additional payouts if you have children under 22 6 ; to help cover caregiver costs 7 ; and to support your dependants when you die 8 .

You are unable to perform at least two (for Singlife CareShield Plus) or three (for Singlife CareShield Standard) of the six Activities of Daily Living (ADLs).

Entering parenthood or purchasing property? Increase your payouts when it matters, without underwriting hassle 9 .

What's severe disability?

A person is considered severely disabled and in need of long-term care when they can’t independently perform at least three of the six Activities of Daily Living (ADLs).

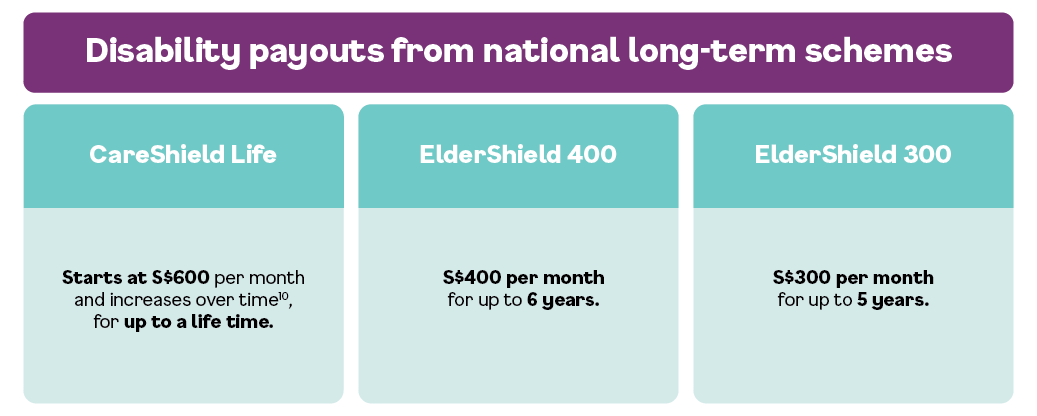

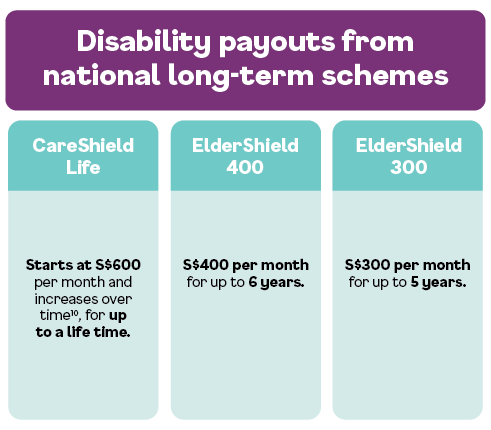

The national schemes at a glance

The CareShield Life and ElderShield schemes give a payout when an individual is severely disabled, i.e. unable to perform three or more ADLs.

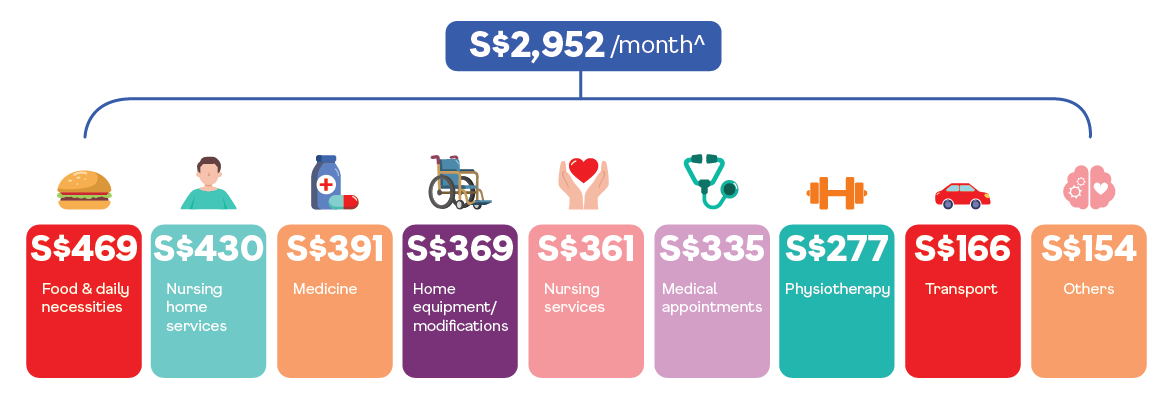

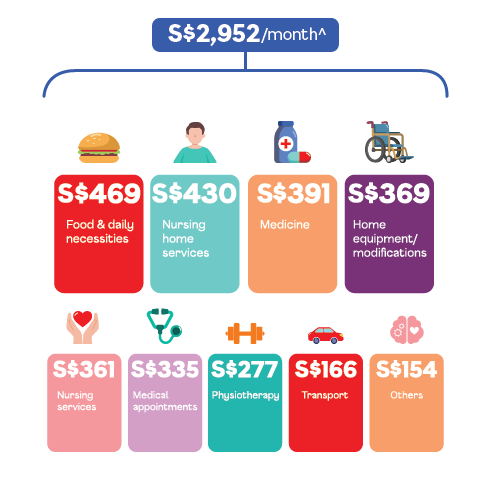

Majority of respondents in Singlife's Long Term Care Research 2024 Study are aware that severe disability could lead to financial and emotional challenges.

Enhance your CareShield Life or ElderShield coverage with Singlife CareShield Standard or Plus to enjoy a 20% lifetime premium discount! Terms and Conditions apply.

Additional discount for MINDEF/MHA/POGISMINDEF/MHA & POGIS insured members and their family will enjoy an additional 20% discount off their first-year premium, on top of the prevailing 20% lifetime discount. Terms and conditions apply.

Singlife Care Collab

A one-stop health services hub offering you convenient access to health care services.

A one-stop holistic care hub, just for Singlife customers

Frequently Asked Questions

What is the minimum and maximum entry age for Singlife CareShield Standard and Plus severe disability insurance plans?

The minimum entry age as at last birthday is 30 and the maximum entry age is 64.

Do I need to have CareShield Life or ElderShield in order to sign up for Singlife CareShield Standard or Singlife CareShield Plus?

Yes, both Singlife CareShield Standard and Singlife CareShield Plus are CareShield Life/ ElderShield supplements, so you need to be eligible for the Singapore government-approved plans.

Do I need a promo code to enjoy the 20% lifetime premium discount for Singlife CareShield Standard and Singlife CareShield Plus?

No, the discount will be automatically applied when you fulfil the promotion criteria during your purchase of these severe disability insurance plans through our website.

All ages mentioned refer to age next birthday (ANB).

1. Deferment Period applies for selected benefits. The Deferment Period is a period of 90 days from the date the Life Assured is confirmed and certified by an Appointed Assessor as being severely disabled. The monthly benefit, Lump Sum Benefit, Dependant Care Benefit and Caregiver Relief Benefit will be paid after the Deferment Period. Waiver of Premium is applicable after the Deferment Period. The Deferment Period shall be waived if the Life Assured suffers from a Severe Disability that arises from the same cause, within 180 days from ceasing to suffer from the Severe Disability.

2. Add-on Benefit payouts start when you’re unable to perform 2 ADLs for Singlife CareShield Standard and 1 ADL for Singlife CareShield Plus.

3. There are two ways to pay for a limited time; the later of the two options will apply. The two ways are:

a) The Life Assured may pay up to the policy anniversary after they turn 68

b) The Life Assured may pay for 20 years from entry age (if Life Assured joins at age 49 or older)

4. MediSave use is applicable to an amount of up to S$600, per calendar year, per life assured. Premiums exceeding this limit will have to be paid in cash. If there are insufficient funds in the designated MediSave account, cash payment will be required for the difference.

5. The monthly benefit refers to the monthly payout when the Life Assured suffers from a Severe Disability, as defined in the plan.

6. The Life Assured may receive an additional 20% of their monthly benefit – for up to 36 months – while they’re receiving their monthly benefit or rehabilitation benefit.

7. The Life Assured may receive an additional 60% of their monthly benefit – for up to 12 months – while they’re receiving their monthly benefit or rehabilitation benefit.

8. A lump sum benefit will be payable if the Life Assured dies due to any accident or sickness while receiving either the Severe Disability Benefit or the Rehabilitation Benefit. The Death Benefit will amount to 3 times of the last paid Severe Disability Benefit or the Rehabilitation Benefit, whichever is applicable.

9. The policyholder may exercise this option, without providing further evidence of insurability at any of the following life stage events, when the Life Assured:

a) purchases a property;

b) marries, divorces or is widowed;

c) becomes a parent by having a newborn child or by adopting a child below 19 years old

d) salary increases by 50% or more from application;

e) completes a skills development course of at least six months;

f ) purchases a new individual life insurance policy or a Supplementary Benefit from us, with full underwriting at standard terms; or

g) spouse suffers a Severe Disability (with the inability to perform at least three of the six ADLs) or dies.

This option allows the policyholder to increase the policy’s monthly benefit with extra premium payable. The total monthly benefit that can be increased under this option is limited to 50% of the policy’s initial monthly benefit, as agreed at policy inception or at the date this option is exercised – whichever is lower. This option is extended to standard life only. Please refer to the Product Summary for more details.

10. Payouts will be reviewed regularly and may be adjusted to account for claims experience and long-term changes in disability and longevity trends

Important Notes Regarding Additional Premium Support (APS) Policy

Anyone who pays for, or is insured under Singlife CareShield Standard/ Singlife CareShield Plus, is not eligible for Additional Premium Support (APS) from the Government*.

If you are currently receiving APS to pay for your MediShield Life and/or CareShield Life premiums, and you choose to be insured under this Singlife CareShield Standard/ Singlife CareShield Plus policy, you will stop receiving APS. This applies even if you are not the person paying for this Singlife CareShield Standard/ Singlife CareShield Plus policy.

In addition, if you choose to be insured under Singlife CareShield Standard/ Singlife CareShield Plus policy, the person paying for Singlife CareShield Standard/ Singlife CareShield Plus will stop receiving APS, if he or she is currently receiving APS.

*APS is for families who need assistance with MediShield Life and/or CareShield Life premiums, even after receiving premium subsidies and making use of MediSave to pay for these premiums.